The report highlights the main updates made to integrate the climate models in order to reflect the most recent climate data and economic outlook on macroeconomic variables, used as part of the models, and consequently, on both physical and transition risks. The impact of those risks varies considerably under each of these scenarios.

For a more detailed overview of the NGFS Phase II scenarios, please refer to our previous publication, NGFS series: Climate scenarios – A range of plausible outcomes. Description and impact of physical and transition risks under each of those scenarios are summarised in our Regulatory guidance on climate and environmental risks for the financial services sector publication.

In this third issue, the NGFS scenarios have been brought up to date with the new economic outlook including COVID-19[1] and climate data, incorporating countries’ policy commitments to reach net-zero emissions made at CO26 in November 2021[2]. As a result, scenarios have been enhanced with more sectoral granularity.

The updates incorporated into the models along with their primary results and impacts are split into three main categories: macro-financial variables, physical (chronic and acute) risk, and transition risk.

Chronic Physical Risks

The NGFS scenarios investigate the impact of chronic physical risks (increase in global mean temperature) on GDP losses. GDP losses from chronic risks vary considerably depending on assumptions about climate sensitivity and the method used to estimate such damages. In the most recent publication, chronic risks are estimated based on a novel damage function methodology[3], using a stylised growth model to extrapolate year-to-year observed damages arising from chronic climate hazards, to illustrate how weather shocks and changes in climate condition (under the scope of the NGFS scenarios, the increase in global mean temperature) affect the macro-financial variables of interest. The latest methodology provides a more precise level of uncertainty (use of the 95th percentile instead of the median) along with results that indicate a much stronger impact on GDP arising from increases in global mean temperature. The current methodology does not include other forms of chronic physical risks and therefore, it is expected that countries or regions exposed to other types of chronic physical risks will show an even higher impact on the reflected macro-financial variable projections.

Acute Physical Risks

Several key factors contribute to the impact of acute physical climate risks including:

- the hazard associated with each risk that a region is exposed to,

- the growing influence of climate change on the associated hazard,

- the exposure of assets to these risks, highly dependent on the geographic location,

- the vulnerability of exposed assets, and

- the mechanisms through which the risks are more apparent at macroeconomic level.

However, it is noted that adaptation can contribute to mitigate these impacts.

The final version of the NGFS scenarios captures for the first time the impact of acute physical risks. This is achieved with the integration of stochastic shocks. Using historical shock data from the Emergency Events Database[4] (EM-DAT), historic economic damages from weather-related natural disasters have been derived to model stochastic shocks for a variation of future trends for acute risks based on the Net Zero 2050, Delayed Transition, and Current Policies scenarios. These damage pathways are used in the National Institute for Economic and Social Research model (NiGEM model) approximating future changes in (in this context GDP).

Source: NGFS Scenarios for central banks and supervisors – Phase III, retrieved from World Bank

Further investigation of the physical risks led to the identification and mitigation of challenges that arose during the process, including limited data and modelling tools. As a result, a six-step methodological framework for extreme physical climate risk assessment was presented along with lessons learned, both summarised below:

- define assessment objectives following a country-specific approach relevant to the data availability, risks, and sectors,

- identify representative data and resources, available at either global or regional level,

- define the scope and approach, including both quantitative and qualitative analysis, refined based on availability of data and modelling tools,

- generate plausible scenarios that explore a range of different effects and shocks though economic sectors, revealing any non-linearities,

- estimate the direct and indirect impact, differing based on the geography, (sub-)sector, and economy, and

- present and interpret results, identify the magnitude of those impacts taking into consideration modelling uncertainty, assumptions, and limitations.

Transition Risks

In terms of transition risk enhancements, the new scenarios are represented with increased granularity for specific sectors, namely the transport and industry sectors, depending on the selected Integrated Assessment Model (IAM).

Regarding the effect of transition risks, the NGFS Phase III publication outlines how the transition due to new policy and regulations and technological developments, will have an impact on greenhouse gas emissions, emissions prices, and energy investments.

Eliminating most greenhouse gas emissions will affect all sectors of the economy. In order to shift away from fossil fuels and carbon-intensive resources, and towards emission-neutral solutions, investing towards green electricity and storage, policy makers can promote this transition by increasing the cost of emission. Transition pathways have been modelled using IAMs[5], which assess the changes needed to be made in order to reach a desirable temperature outcome or carbon budget (known as shadow carbon price). The shadow emissions price is a proxy for government policy intensity and changes in technology and consumer preferences and constitutes a key indicator of the level of transition risk underlined in each scenario. Shadow emission prices depend on the stringency of policy, timing of implementation, distribution of policy measures across sectors and geographies, and technological development assumptions such as, the availability of carbon dioxide removal technologies, which is overall assumed low to medium in the presented NGFS scenarios.

Macro-financial Variables

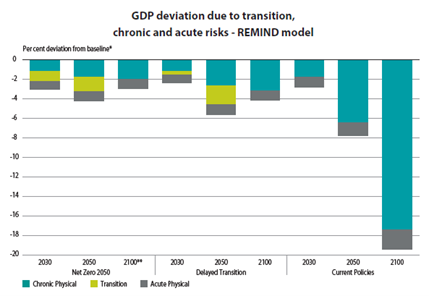

Scenarios differ significantly in their economic impact, with physical risks outweighing transition risks under all scenarios and time scales, both varying across different geographic regions. The NiGEM model provides country and regional pathways for GDP under each of the climate-scenarios. Impacts are higher for countries and regions that face higher emissions reduction, higher carbon prices, lower fossil fuel exports, and/or higher physical risk damages. It is noted that the GDP losses trajectories also vary across the three IAMs, depending on model structure and assumptions.

Source: NGFS Scenarios for central banks and supervisors – Phase III

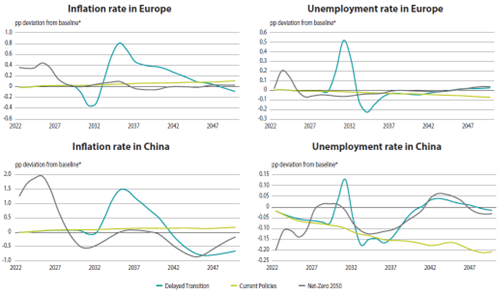

In the final publication, the scenarios included a wide range of macroeconomic variables, capturing the relationship between key macros such as, inflation and unemployment, and the scenarios. It is noted that the observed trends (modest increase in inflation and unemployment rates with rise of carbon prices) are primarily driven by carbon prices as part of the transition scenarios. Further research needs to be made on the current results, to better model the potential physical risks, in order to examine further the impact of physical risks on key macroeconomic variables. For example, since Current Policies scenario impacts are vastly dependent on physical risks with limited transition risks, assuming slow technological change and minimal policy implementation, limited modelling of physical risks will be unable to capture the correct trend.

Source: NGFS Scenarios for central banks and supervisors – Phase III

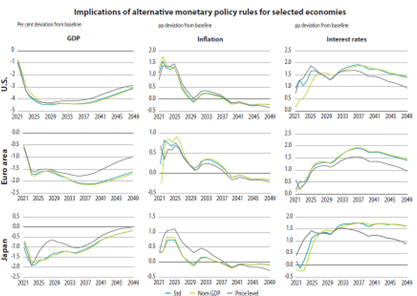

Source: NGFS Scenarios for central banks and supervisors – Phase III

Outcomes and Future Objectives

The NGFS scenarios have been developed to provide a common starting point for analysing climate risks to the economy and financial system in order to identify any potential future risks, and to prepare the financial system for the shocks that may arise. Reaching global net zero CO2 emissions by 2050 will require an ambitious transition across all sectors of the economy. Immediate coordinated transition will be less costly than disorderly transition or inaction in the long run.

In future publications, the NGFS aims to improve the design of the scenarios (including increased sectoral granularity and geographical coverage, short-term scenarios that can be used as part of scenario analysis and stress testing, and better representation of physical risks) and broaden their range of usage providing users with methodological guidance to apply the scenarios in practise.

Grant Thornton’s Quantitative Risk offerings

The Grant Thornton Quantitative Risk Advisory Team has a proven track record of success in meeting the most challenging of tasks for Institutions, local banks, and other Financial Services companies.

[1] Current data do not yet account for the war in Ukraine as the situation and its outcome is still unclear and therefore difficult to model.

[2] The 2021 United Nations Climate Change Conference, more commonly referred to as COP26, was the 26th United Nations Climate Change conference, held at the SEC Centre in Glasgow, Scotland, United Kingdom, from 31 October to 13 November 2021.

[3] Kalkuhl, M., & Wenz, L. (2020). The impact of climate conditions on economic production. Evidence from a global panel of regions. Journal of Environmental Economics and Management.

[4] Emergency Events Databased (EM-DAT)

[5] The transition pathways were produced by three IAM teams: PIK (REMIND-MAgPIE model), IIASA (MESSAGEix-GLOBIOM model) and UMD (GCAM model).