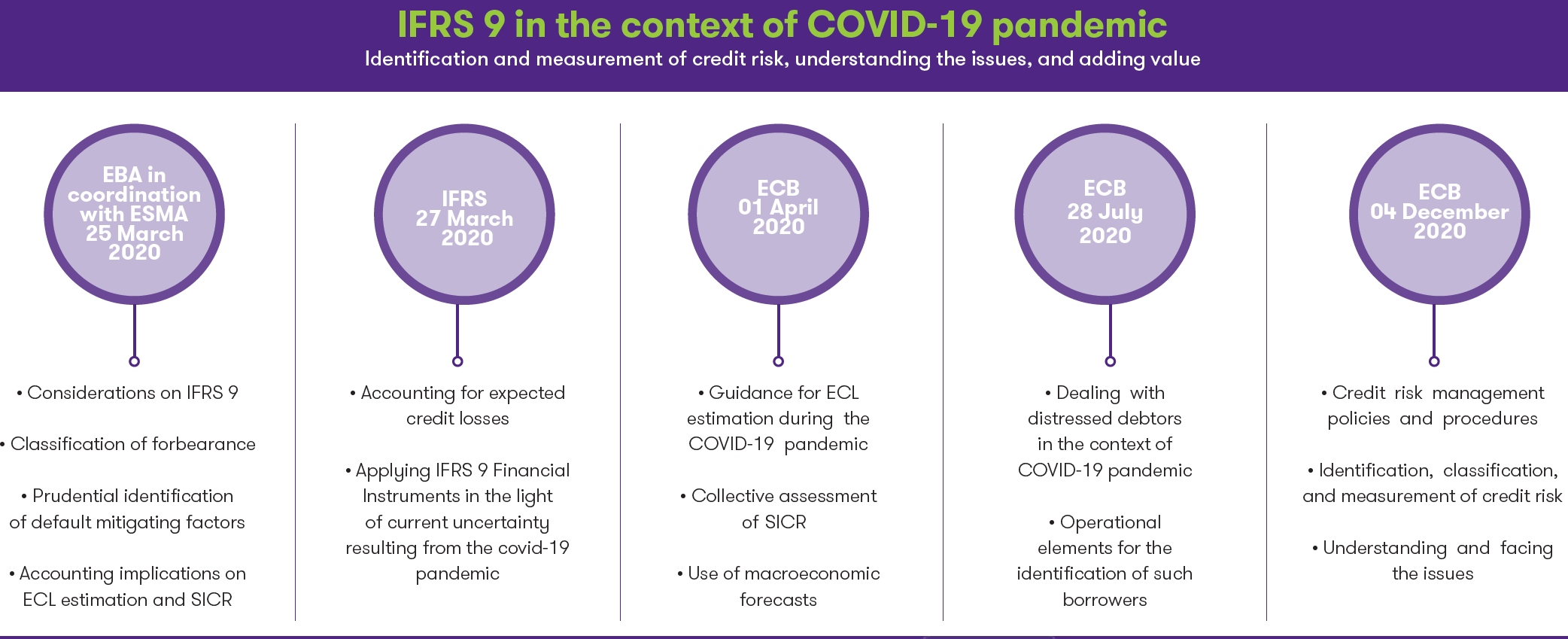

Following the uncertainty arising from the current economic shock, prudential and securities regulators have published guidelines for the application of IFRS 9 in the context of the COVID-19 pandemic.

Contents

Significant Institutions are expected to follow these guidelines for the estimation of Expected Credit Loss (ECL) and the assessment of Significant Increase in Credit Risk (SICR) in accordance to IFRS 9 accounting for the implications emerging from the COVID-19 outbreak. Understanding the potential issues in the identification, classification and measurement of credit risk is vital for the timely mitigation of potential challenges.

Our aim as a team is to provide detailed, actionable insight that incorporates industry best practice and standards to enable you to strengthen your procedures for forecasting credit risk in the context of COVID-19.