Transfer pricing: new rules as of 1 January 2022

Tax update

By: George Karavis

12 Jul 2022 3 min read

The Cyprus parliament amended Article 33 of the Income Tax Law concerning Transfer Pricing, and at the same time issued regulations concerning the application of the new Transfer Pricing legislation. Furthermore, the Cyprus parliament amended the Assessment and Collection of Taxes Law in order to incorporate the relevant penalties in case of non-compliance with the new Transfer Pricing documentation requirements.

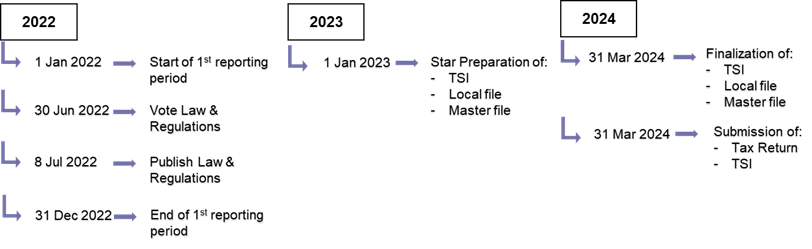

The law and regulations have been published in the Government Gazette on 08 July 2022 and are effective from 1 January 2022.

In summary

The new transfer pricing law and regulations cover all types of transactions between related parties in excess of €750.000 per category of transaction.

Type of transactions:

-

- Goods: Sale and purchase of goods

- Services: Provision and receipt of services

- IP Related: Sale, purchase, leasing of intangible assets

- Financing: Provision and receipt of financing

- Other: Any other transaction between controlled parties.

The related parties that meet the threshold of €750.000 per category of transaction, have obligation to prepare a Master File, Local File and the Table of Summarized Information (“TSI”).

-

- The TSI: should be prepared and submitted annually to the Tax Authorities along with the Tax Return of the taxpayer (no threshold applies)

- The Local File: should be prepared by all taxpayers involved in controlled transactions before the tax return filing deadline

- The Master File: should be prepared by all taxpayers involved in controlled transactions before the tax return filing deadline. It applies only to companies that are ultimate or surrogate parent entities of multinational group which has consolidated revenues above €750M (with CbCR obligations).

What’s New

Amended Article 33

The following provisions have been incorporated into the amended Article 33 of the Income Tax Law:

- One of the most important developments of the amended Article 33, is the incorporation of the arm’s length principle, which should be applied and interpreted in accordance with the OECD Transfer Pricing Guidelines for Multinational Entities and Tax Administrations

- There is also a significant amendment to the definition of connected parties. More specifically, the amended Article 33 introduces the 25% relationship test

- Furthermore, a new Article 33C was incorporated in the legislation allowing the taxpayers to apply for an Advance Pricing Agreement (“APA”)

- Lastly, the amended Article 33 makes reference to the Regulations that are issued by the Council of Ministers (see New Regulations paragraph below).

New Regulations

The Council of Ministers issued the following Regulations, providing guidelines and further information about the:

A. Transfer Pricing Documentation Requirements

Providing more details about the Local file, Master file and TSI, including deadlines, their content and the persons who are allowed to undertake an assurance quality review of the Local file.

B. Advanced Pricing Agreement (“APA”)

Providing more details about the application procedure for an APA.

Exemptions

Related parties with controlled transactions below €750.000 per category of transaction, are exempt from the provisions of the amended Article 33 of the Income Tax Law (i.e. they do not have an obligation to prepare and submit a Master File, Local File and TSI).

Timeline Penalties

Penalties

The penalties vary between €500 - €20.000 depending on the delay in filing.

|

|

Penalty |

|

Non-submission of TSI within deadline |

€500 |

|

Late filing of the Local &/or Master File:

|

€5.000 €10.000 €20.000 |

Next steps for the Taxpayers

- assess the impact of the new legislation and regulations to your business (i.e. transactions with connected parties above €750.000 per category, per annum)

- consider the preparation of a Transfer Pricing Study before the tax return filing deadline, to ensure that the transactions with connected parties are at arm’s length

- consider the preparation of a Local file, Master file and TSI before the tax return filing deadline

- remember to submit the TSI to the Tax Authorities along with the Tax Return (same filing deadline with the tax return)

- keep books and records for at least six years from the end of the relevant tax year.

How we can help

We are at your disposal to discuss the potential impact of the new legislation and regulations to your business. We can also assist you with the new compliance requirements including:

- preparation of a Transfer Pricing Study

- preparation of Local file, Master file and TSI

- review and certify the quality of a Local file.

Authors