It will comprise several phases including data collection, quality assurance, and the computation of results, aiming to identify vulnerabilities, industry best practices, and the challenges faced by banks. The exercise is expected to help enhance data availability and quality gathered by the banks. The output of the stress test exercise will be integrated into the Supervisory Review and Evaluation Process (SREP) using a qualitative approach. ECB’s climate stress test methodology is indicative, with no direct implications linked to the bank’s capital requirements. The results of this stress test exercise will provide the regulator with insights into the bank’s climate risk exposures, which might affect the Pillar 2 requirements via the SREP scores. The stress test consists of three distinct modules.

1. Qualitative questionnaire

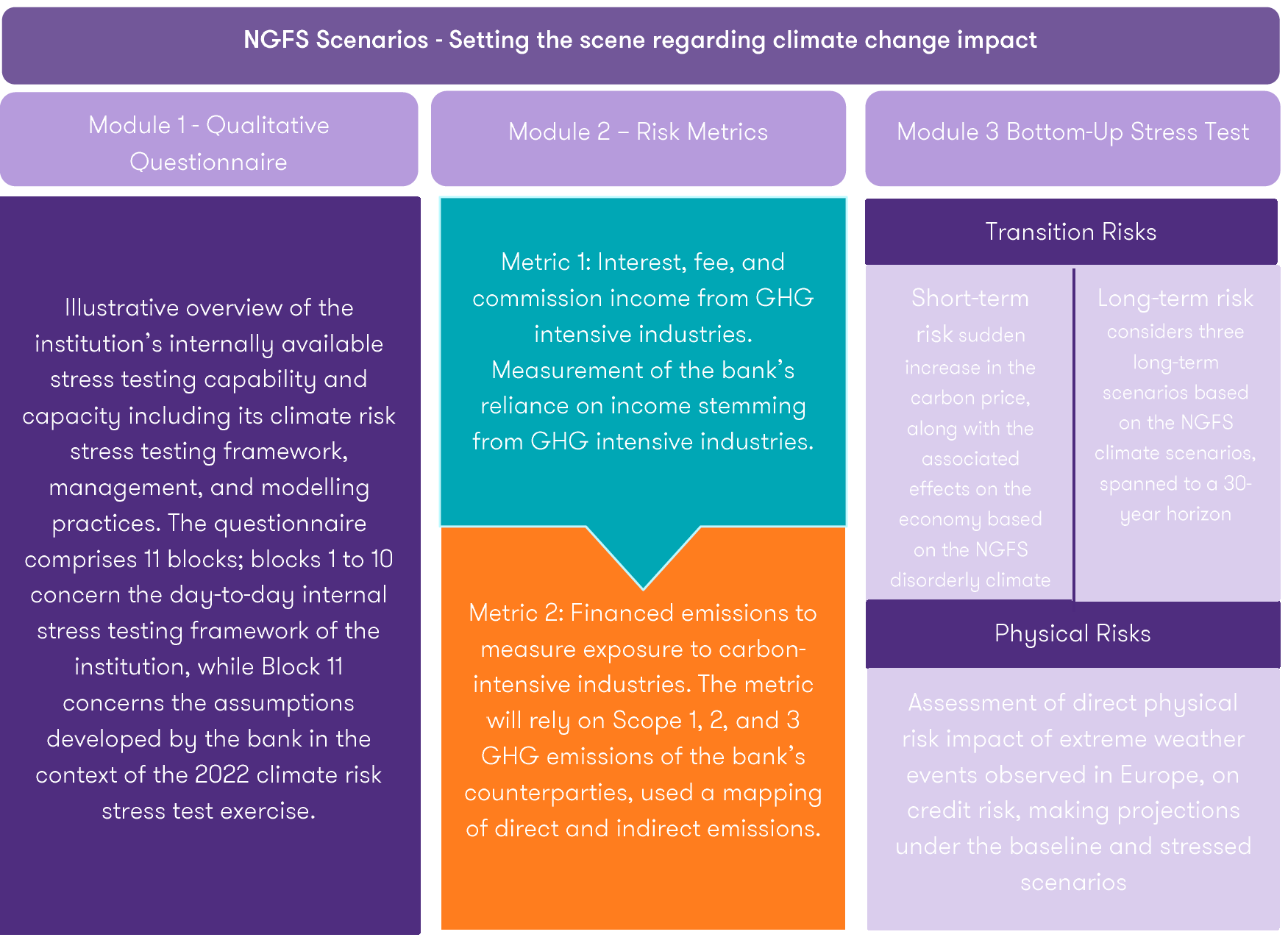

The purpose of this module is to gain an illustrative overview of the institution’s internally available stress testing capability and capacity including its climate risk stress testing framework, management, and modelling practices. The questionnaire comprises 11 blocks; blocks 1 to 10 concern the day-to-day internal stress testing framework of the institution, while Block 11 concerns the assumptions developed by the bank in the context of the 2022 climate risk stress test exercise. The questions in the first ten blocks of the survey and specific questions of Block 11 are mandatory for all participating banks. The remaining questions in Block 11 are only mandatory for banks that provide projections in the bottom-up stress test for Module 3 – Bottom-Up Stress Test Projections.

2. Climate risk metrics

In the 2022 climate risk stress test exercise, all banks are requested to provide a set of common climate-related metrics. The metrics have been designed to shed light on banks’ analytical and data capabilities regarding climate risk. Banks are asked to split the corporate exposures of their portfolio into 22 pre-defined NACE based industries.

- Metric 1: Interest, fee, and commission income from greenhouse gas intensive industries

The reported information will be used to construct various metrics to measure the bank’s reliance on income stemming from GHG intensive industries and provides a proxy for the sustainability of the bank’s business model. The reference period for the income and expenses data collection is the sum of the time-weighted notional of all instruments that were on the bank balance sheet from 1 January 2021 to 31 December 2022.

- Metric 2: Financed greenhouse gas emissions

To measure exposure to carbon-intensive industries, each bank is expected to provide the necessary data to calculate a weighted average GHG intensity metric. This will provide an indication of the climate-related risk in the bank’s non-financial corporations portfolio. The metric will rely on Scope 1, 2, and 3 GHG emissions of the counterparties. Scope 1, 2, and 3 GHG emissions provide important information for the mapping of direct and indirect emissions.

3. Bottom-up stress test projections

This section describes the methodology and requirements for the starting point data and projections that institutions must provide for the bottom-up stress test exercises targeting transition and physical risks. The 2022 Single Supervisory Mechanism (SSM) climate risk stress test does not cover all the transition and physical risk channels as defined in the ECB Guide on climate-related and environmental risks.

Transition risk

This stress test covers banks’ potential financial losses in both short-term and long-term transition risk scenarios. The exercise is assessing the institutions’ short-term vulnerabilities under a three-year disorderly transition scenario triggered by a sharp increase in the price of carbon emissions and the long-term strategies under three different transition scenarios over a 30-year horizon.

The credit risk exposures in scope are an institution’s mortgage and corporate exposures. Banks are requested to split their corporate exposures in 22 pre-defined NACE industries and mortgage exposures by Efficiency Performance Certificate (EPC) rating. In regard to market risk exposures, banks are requested to classify their bond and stock holdings by the same 22 NACE industries as in credit risk. Banks are also requested to provide starting point values broken down by country and portfolio as of 31 December 2021.

Methodological approach: short-term tail risk. The exercise is inspired by the disorderly transition scenario developed by the Network for Greening the Financial System (NGFS). However, this exercise assumes that the increase in the carbon price will occur in 2022, along with the associated effects on the economy, and not in 2030 as indicated by the NGFS disorderly scenario. The aim of this hypothetical risk event is to assess the sensitivity of banks’ current balance sheets to unexpected sharp measures on cutting down carbon emissions in the near term.

Methodological approach: long-term strategic response. This exercise considers three long-term scenarios based on the NGFS climate scenarios, spanned to a 30-year horizon. Banks are requested to outline their strategies under these three scenarios, projecting their mortgages disaggregated by EPC and corporate exposures disaggregated by industry for reference dates at 10-year intervals i.e., 2030, 2040, and 2050. The focus of these long-term projections is on obtaining detailed insights into the resilience of banks’ business models and their adaptability in different long-term transition scenarios.

Physical risk

The assessment of physical risk will focus on the direct impacts of two extreme weather events in Europe; large floods and severe droughts and heatwaves, on credit risk.

Regarding severe droughts and heatwaves, banks are requested to classify their credit exposures to counterparties broken down by NACE sector code, while the flood stress map is used to split credit exposures impacted by flood risk. The map disaggregates regions into no risk, low risk, medium risk, and high-risk areas. Starting point values for credit risk exposures and credit risk parameters, should be gathered as at 31 December 2021.

For both types of physical risks, banks are asked to calculate both baseline projections (i.e., without the flood or drought and heatwave) and stressed projections incorporating the flood or drought and heatwave scenario. In order to calculate the baseline projections, banks can use the macroeconomic projections from the December 2021 Eurosystem BMPE to the extent needed for their models.

How we can help

Our Prudential Risk, ESG experts, and consulting team understands that regulation continues to drive the strategic agenda for banks and investment firms. ESG and other sustainability related areas are likely to be high on the regulatory agenda for years to come. We specialise in assisting clients across the financial services sector in navigating through the maze of regulation and support clients to identify regulatory obligations and work towards full compliance balanced with your business needs.