As part of the advisory process, we ask questions and pay attention to your responses. Rather than relying on off-the-shelf services that could loosely fit a...

We approach each audit with sharp thought, straight talk and common sense. In addition to verifying that financial results are fairly presented and meet...

Change and ongoing transformation are fundamental requirements for success in the 21st century. The Grant Thornton Business Consulting team supports...

As organisations become increasingly dependent on digital technology, the opportunities for cyber criminals continue to grow.

-

Privacy and Data Protection

Our digital risk team is made up of a combination of subject matter experts and technical specialists who can help your business comply with the GDPR.

-

Governance, Risk and Compliance (GRC)

While business goals and strategies evolve, our services support you wherever you are in your business cycle. The digital economy is simultaneously increasing the magnitude of new business opportunities while increasing the difficulty of getting it right.

-

ISO 27001 and ISO 27701

Grant Thornton’s ISO 27001 and ISO 27701 specialists will arrange and oversee the formal audit process.

-

SOC 1,2,3

As a service organization there are many ways to provide assurance to your customers and in turn other stakeholders over your control environment. One of the most effective and cost-efficient ways is to issue a Service Organization Control (SOC) Report.

-

Incident Response

Grant Thornton’s Cyber Incident Response Team can support your business in the event of a cyberattack or data loss event. We work alongside your existing IT and Legal teams to provide a co-ordinated, timely and efficient investigation and remediation.

-

Hacking Services

At Grant Thornton, our cyber security experts can develop a bespoke penetration testing plan to meet your business needs and unique IT environment. We can undertake the full suite of testing or conduct individual assessments, as required.

-

Cyber Health Check

Approximately 54% of organizations report that they have experienced at least one cyber-attack during the past year. Grant Thornton’s cyber health check provides you with an objective, jargon-free assessment of your current cyber security, drawing on both qualitative and quantitative elements.

-

Dark Web Threat Intelligence

We use a variety of dark and deep web monitoring tools that continuously scans illegal sites to discover any mention of your data, ranging from breached security credentials such as usernames and passwords to leaked confidential documents of your company.

-

Digital forensics and electronic discovery

We offer a full suite of digital forensics and data acquisition services in investigations related to cybercrime, disputes, fraud and regulatory investigations.

Technology has transformed how we work, play, and do business. It has provided new solutions to old problems, disrupted traditional business models, and...

In all of our work our principal purpose is to preserve or create value for stakeholders. To achieve this, we utilise solutions that cover the following...

-

Insolvency

If you're facing a time of personal or corporate financial crisis you need advice from someone who listens, who understands your specific issues and deals with them in a supportive and sensitive manner.

-

Crisis stabilisation and turnaround

In periods of financial distress, management teams often face considerable challenges, with many directors having little or no experience of similar conditions.

-

Operational and financial restructuring

Companies challenged by underperformance often need support in identifying options for financial or operational restructuring. Tapping this type of advice helps them create a stable platform for business turnaround.

-

Accelerated M & A

Even fundamentally sound businesses run into difficulties. Cash flow can come under pressure from the loss of a big client, or a dip in performance can threaten a breach of banking covenants if there is insufficient headroom.

Outsourcing your operations and specific business functions to Grant Thornton can not only cut costs, but also bring new insights and experience to your...

Focusing on people to drive your business forward

At Grant Thornton, we believe that people are the cornerstone of any successful business, whether it's a...

-

People Services

Our HR Outsourcing solutions are designed to provide you with the flexibility and expertise needed to manage your people effectively and efficiently.

-

Relocation made easy!

We bring to the table our in-depth understanding of Cyprus immigration legislation and policies, coupled with long experience supporting corporate clients relocating non-EU staff to Cyprus, as well as entrepreneurs and executives moving with their families.

-

Family Office Services

In an era of rising digital threats, protecting the sensitive information and assets of high-net-worth families is paramount. In collaboration with our dedicated strong Cybersecurity and Data Protection team, we can help ensure the data security and privacy of your Family Office (employees and c-suite), family members and any staff supporting them, and also trusted associates.

-

Client Vacancies

As part of our People, Relocation and Family Office Services, we support our clients in finding talent to meet their unique needs. Here, you’ll find open positions available within our clients’ businesses across a variety of industries. Browse the opportunities below to see how you can become part of their teams!

Our Financial Services Advisory team provides market-leading risk, advisory, project management and consulting services for the largest and most important...

Grant Thornton Cyprus understands the regulatory landscape and works closely with clients to understand their strategy and benchmark their performance against...

View our risk and compliance services.

Sustainability

At Grant Thornton, tax is a key part of our organisation and our award-winning teams can offer you a range of solutions, whatever the size of your business or...

-

Indirect Tax

Our experienced VAT specialists are available to assist companies and entrepreneurs of all industries and sizes in meeting their obligations.

-

Direct Tax

We can help you ensure a bespoke balance between tax compliance and effective tax planning for your special circumstances.

At Grant Thornton Cyprus’ AI and Data Lab, we help businesses unlock the hidden value of their data, empowering them to make smarter decisions, innovate...

Energy and resources markets worldwide are undergoing major changes. With growing energy demand, developments in new forms of energy and the need to invest in...

Emerging markets and shifting consumer demand are creating new opportunities in consumer products, with business leaders investing in new products, markets and...

Optimism is slowly returning to the global economy, but the financial services industry needs to regain the trust of public and private bodies. To succeed,...

Across the globe, not for profit organisations are increasingly expected to deliver more, while at the same time facing cuts in government funding and...

We work with all types of agencies, including central and state government, local government, donors (including bilateral and multilateral international...

While the impact of the prolonged downturn continues to be felt, pockets of opportunity and optimism have emerged within the retail estate and construction...

Dynamic businesses need to move with speed and purpose if they want to capitalise on opportunities in hospitality and tourism. At Grant Thornton, we know...

Rapid change and complexity are norms, and innovation the fuel in the technology industry. Today’s revolutions – including cloud, as-a-service, social media...

With our unique culture and opportunities, our organisation is a place where you can grow.

If you know a high-school student who's curious about Artificial Intelligence, they should definitely check out the GT AI Summer Bootcamp 2025. It’s a dynamic...

Are you ready to jump into the world of computer security and put your problem-solving skills to the test? We're thrilled to announce our upcoming three-day...

This unique programme was specifically designed by Grant Thornton Cyprus for highschool students (currently in year 5 or 6).

At Grant Thornton, talented people are at the heart of our strategy and drive all of our successes.

-

Ημερίδα Γνωριμίας με την Grant Thornton Κύπρου

Σας προσκαλούμε σε μια μοναδική ευκαιρία να γνωρίσετε την Grant Thornton Κύπρου! Την Τρίτη, 5 Νοεμβρίου 2024, θα έχετε τη δυνατότητα να συναντήσετε την ομάδα μας, να ενημερωθείτε για επαγγελματικές ευκαιρίες και να εξερευνήσετε πιστοποιήσεις όπως ACCA.

-

Life at Grant Thornton

At Grant Thornton Cyprus, we are taking a holistic approach and reimagining the way we work, continually assessing it and making necessary changes to better support our people.

-

In the community

Unlocking the potential for growth in our local communities.

-

Diversity and inclusion

Diversity helps us meet the demands of a changing world. We value the fact that our people come from all walks of life and that this diversity of experience and perspective makes our organisation stronger as a result.

-

Global talent mobility

One of the biggest attractions of a career with Grant Thornton Cyprus is the opportunity to work on cross-border projects all over the world.

-

Learning and development

At Grant Thornton we believe learning and development opportunities allow you to perform at your best every day.

-

Our values

We are a values-driven organisation and we have more than 56,000 people in over 140 countries who are passionately committed to these values.

Grant Thornton offers something you can't find anywhere else. This is the opportunity to develop your ideas and thinking while having your efforts recognised...

Grant Thornton can give you a flying start. We are ambitious. Take the fact that we're the world's fastest-growing global accountancy organisation.

Quantitative risk

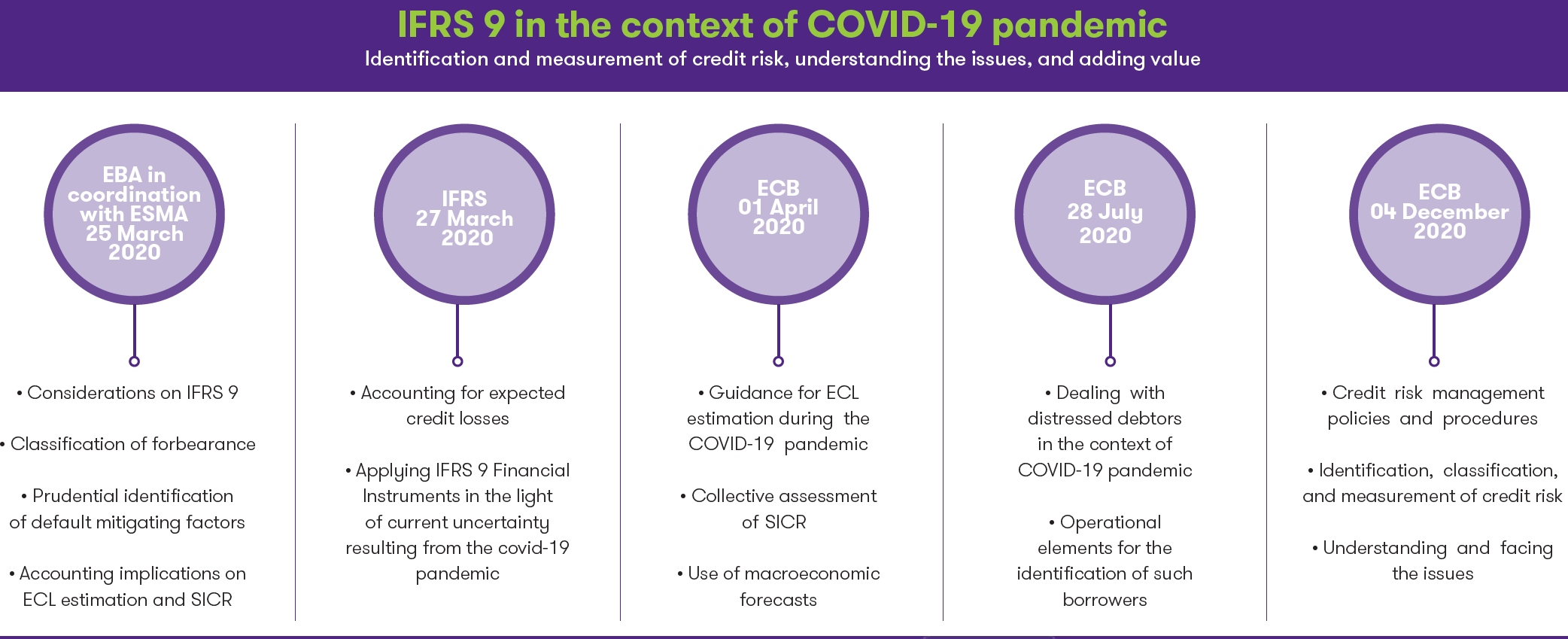

IFRS 9 in the context of COVID-19 pandemic

Following the uncertainty arising from the current economic shock, prudential and securities regulators have published guidelines for the application of IFRS 9 in the context of the COVID-19 pandemic.

Contents

Significant Institutions are expected to follow these guidelines for the estimation of Expected Credit Loss (ECL) and the assessment of Significant Increase in Credit Risk (SICR) in accordance to IFRS 9 accounting for the implications emerging from the COVID-19 outbreak. Understanding the potential issues in the identification, classification and measurement of credit risk is vital for the timely mitigation of potential challenges.

Our aim as a team is to provide detailed, actionable insight that incorporates industry best practice and standards to enable you to strengthen your procedures for forecasting credit risk in the context of COVID-19.

Authors

-

Andreas Spyrides Andreas is leading the Quantitative Risk at Grant Thornton (Cyprus) Ltd and he is the Head of the subsidiary company Grant Thornton Quantitative Risk (Cyprus) Ltd.

Andreas Spyrides Andreas is leading the Quantitative Risk at Grant Thornton (Cyprus) Ltd and he is the Head of the subsidiary company Grant Thornton Quantitative Risk (Cyprus) Ltd.View Profile